Andy Powers-A Professional who cares..About YOU!

Social Security/Medicare “Entitlements” cut by Bipartisan Budget Act of 2015

In the fall

of 2015, rather than better manage government budgets as would do a business, in

order to mitigate the out of control national budget deficit, now approaching

$19 TRILLION, our Congress, elected by us to represent our best interests, voted

to cut social security benefits and increase Medicare Premiums. First, these are

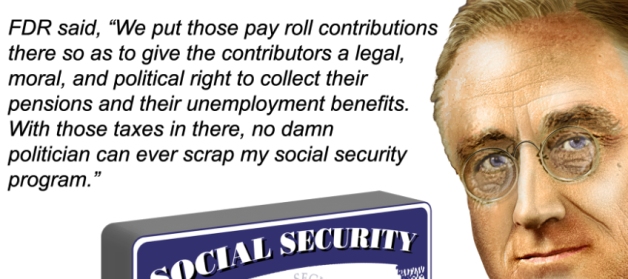

NOT entitlement benefits. They are “insurance” benefits, which workers and their

employers paid “deemed premiums” for decades. A private insurer would not be

permitted to do this, as when we paid the first mandatory “premium” (IE

Consideration), we entered into a contract with the U.S. Government that in

exchange workers would be entitled to insurance benefits in the form of social

security and Medicare. Remember that Social Security was legislated pursuant to

the Federal Insurance Contribution Act of 1935 and Medicare added in 1964.

In the fall

of 2015, rather than better manage government budgets as would do a business, in

order to mitigate the out of control national budget deficit, now approaching

$19 TRILLION, our Congress, elected by us to represent our best interests, voted

to cut social security benefits and increase Medicare Premiums. First, these are

NOT entitlement benefits. They are “insurance” benefits, which workers and their

employers paid “deemed premiums” for decades. A private insurer would not be

permitted to do this, as when we paid the first mandatory “premium” (IE

Consideration), we entered into a contract with the U.S. Government that in

exchange workers would be entitled to insurance benefits in the form of social

security and Medicare. Remember that Social Security was legislated pursuant to

the Federal Insurance Contribution Act of 1935 and Medicare added in 1964.

Here are two ways we were screwed by our elected “representatives” with the “BBA2015”. First the “file and suspend” option, enacted in 2000, was repealed. This enabled an older spouse who as FRA and the greater earner, to file for benefits at FRA and immediately suspend the benefits, while a younger spouse age 62 or older could have increased his or her benefits if their personal SS benefits were lower. Next the BBA2015 eliminates the “restricted application” (a strategy for decades) whereby if filed in combination with the “file and suspend” election, would enable one spouse at FRA to receive “50% spousal benefits”, enabling personal SSA benefits to accrue an annual 8% increase each year between age 66 and 70.

Beside the fact that our legislators our permitted to claw back benefits that we paid for pursuant to a mandated contract with the government, this is most frustrating for those who planned their retirement benefits prior to the enactment of the 2015 legislation and faced with losing tens of thousands of dollars. Worse yet is that those who have been rushing to the Social Security Administration office to implement a file and suspend prior to the April 29 deadline, many are being denied and being given totally incorrect information and being turned away by the clerks on the SSA payroll, funded by our tax dollars (and lost benefits).

Three good articles targeting this topic can be found from T Rowe Price at http://individual.troweprice.com/retail/pages/retail/applications/investorMag/2014/june/managing-it/index.jsp; Time Inc. at http://time.com/money/4158806/social-security-benefit-file-suspend/ and Investment News http://www.investmentnews.com/article/20160217/BLOG05/160219941/some-local-social-security-administration-offices-refuse-to-process.

Another way baby boomers are being screwed is because those born after 1951 and waiting for 2016 or later to begin health coverage under Medicare (along with taxpayers) will find themselves paying higher Medicare B premiums. And with Obamacare exchange programs going bankrupt, baby boomers will end up paying higher Medicare D premiums and higher supplemental insurance premiums (along with all other health care insurance premiums). US News http://money.usnews.com/money/blogs/planning-to-retire/2015/11/20/some-retirees-pay-higher-medicare-premiums-in-2016 by Andy Powers, Mahopac N.Y.